Investing in Brokered Certificates of Deposit

Brokered CDs offer the comfort of FDIC insurance

If an investor’s primary goals include principal preservation and income, brokered certificates of deposit (CDs) can serve as a sound portfolio foundation.

This week’s negotiable CD rates:*| 3-mos. | 6-mos. | 9-mos. | 1-year | 2-year | 3-year | 4-year | 5-year |

|---|---|---|---|---|---|---|---|

| 5.45% | 5.40% | 5.40% | 5.30% | 5.00% | 4.85% | 4.65% | 4.55% |

As of June 20, 2024, annual percentage yields (APY) represents the interest earned based on simple interest calculations. Rates are subject to change and availability. Minimum purchases may apply.

* Please read the CD Disclosure Document.

Brokered CDs may be a good investment in a balanced portfolio, and it’s important to understand all the benefits and risks.

Certificates of Deposit (CDs) are promissory arrangements between a depositor/investor and a bank, whereby the issuing bank agrees to pay a predetermined rate of interest in exchange for the investor agreeing to deposit funds for a fixed period of time.

Brokered CDs offer:

FDIC protection

CDs are insured by the Federal Deposit Insurance Corporation up to a predetermined limit, based on account category. More details are available on fdic.gov.

Flexibility in length of investment

We offer a wide range of maturities to help match an investor’s investment objectives. Upon maturity, the proceeds are deposited into the account and become available for subsequent investment opportunities.

Choice of cash flow

Short-term CDs, one year or less, typically pay interest at maturity, while longer-term CDs offer monthly, quarterly or semiannual interest payments. Interest is not compounded and payments become available for withdrawal.

Liquidity prior to termination

If the need for cash arises before the maturity date, CDs may be liquidated in the secondary market at prevailing market prices, which may be more or less than an investor's original purchase price.

Survivor’s option

Brokered CDs offer an estate protection feature, which allows the estate or the beneficiary, upon the death of the holder(s), to redeem CDs from the issuer at par plus accrued interest without incurring a penalty, subject to limitations. Irrevocable trusts do not offer a survivor's option.

Before exercising the survivor's option, an investor should determine whether CDs are trading at a premium in the secondary market. If the secondary market value is above par, then it may be more beneficial to sell CDs at a higher price rather than redeem from the issuer at par.

Comparing bank and brokered CDs

Not all CDs need to be purchased directly from banks. An investor can choose to buy CDs either directly from a bank or through a brokerage account. However, there are differences between traditional bank CDs and brokered CDs, so investors should carefully consider the characteristics of each in order to choose the most appropriate alternative for their individual circumstances.

Brokerage firms receive a placement fee from the issuer in connection with your purchase of a CD in the primary market. Secondary market transactions may also include fees associated with facilitating such a transaction.

| Bank CDs | Brokered CDs | |

|---|---|---|

|

FDIC Insurance |

FDIC-insured up to $250,000 in principal and interest per financial institution per beneficial owner. |

FDIC-insured up to $250,000 in principal and interest per financial institution per beneficial owner. |

|

Length of Investment |

Usually short-term alternatives. |

Wide range of maturities to match investor investment objectives. |

|

Returns |

Rates are locked until maturity. Return is quoted as Annual Percentage Yield* (APY), which includes the compounding of interest. |

Rates are locked until maturity. Some CDs offer variable rates that change during the term. Return is quoted as Yield to Maturity* (YTM). Interest is not compounded – also known as simple interest. Some CDs may be callable prior to maturity at issuer’s option, which may affect your total return. |

|

Interest Payments |

Interest is usually paid at maturity. |

Interest is paid at predetermined intervals, such as monthly, quarterly, semiannually or at maturity. |

|

Liquidity |

Early withdrawals with penalty are usually permitted. |

May be sold in the secondary market at prevailing market prices. Proceeds may be more or less than the original investment as prices are sensitive to changes in interest rates. |

|

Estate Protection |

Varies by issuer. |

CDs offered through Raymond James offer a Survivor’s Option, which allows the estate, upon the death of the holder(s), to redeem CDs from the issuer at par plus accrued interest. Irrevocable trusts do not offer a survivor's option. |

|

Other Features |

Upon maturity, proceeds are generally automatically reinvested, unless the investor opts out. |

Neither interest payments nor the principal are automatically reinvested, which allows investors to choose from a variety of investment opportunities. |

*On a new issue brokered CD, APY and YTM are generally the same.

Brokered CD variations:Callable brokered CDs

At times, banks may offer CDs with an option to call or redeem them prior to the stated maturity date. The call option is at the option of the bank and not the investor. The call schedule is determined at the time of issuance, and CDs may not be called before the first call date.

Callable CDs are more likely to be called in a lower interest rate environment, and investors may be unable to reinvest funds at the same rate as the original CD.

Banks typically offer higher interest rates on callable CDs than on non-callable CDs in order to compensate investors for a potential risk of a call. Because calls are not mandatory and cannot be predicted, investors should consider multiple scenarios when analyzing the potential total return of callable CDs.

Step-up CDs

Step-up CDs offer coupon rates that increase based on a predetermined schedule. The initial interest rate may be lower than the interest rate paid on comparable fixed-rate CDs. However, the consequent increase in coupon payments may result in a higher overall return at maturity. Step-up CDs are generally issued with a call feature, which is at the option of the bank, with the step-up schedule coinciding with the call schedule. If CDs are not called, the coupon rates will step up to the next predetermined level. The step rate may be below or above then-prevailing market rates. The investor may be accepting a lower current coupon than a comparable fixed rate bond for the possibility of higher coupons in the future (if not called).

Floating-rate CDs

Floating-rate CDs adjust their coupon payments by a predefined percentage, or spread, over the reference rate, such as the Consumer Price Index (CPI). The rate of return on a floating-rate CD will depend on changes to its reference rate. Consequently, the initial rate cannot be used to calculate the yield to maturity.

It is important to compare the risks and benefits of each investment alternative to determine which is most appropriate, based on portfolio objectives.

Investment Considerations

FDIC protection

All CDs offered through Raymond James are insured by the FDIC up to $250,000 for all deposits held in the same capacity at one bank. Insurance limits are determined based on account ownership category.

Additional Insurance Protection

Raymond James offers brokered CDs from multiple financial institutions across the country. By purchasing CDs from several banks, an investor can easily keep the entire CD portfolio insured even if it exceeds $250,000.

Keeping track of insurance limits

As an investor, it is important to track total deposits – CDs, checking, savings, trust and money market deposit accounts – to ensure they do not exceed the FDIC insurance limit of $250,000 at any one bank.

Banks often have similar names, so check each bank's FDIC certificate number, which identifies each bank as a separate institution. FDIC certificate numbers are available at fdic.gov. A detailed explanation of insurance limits is also available at fdic.gov or by phone at 877.ASK.FDIC (877.275.3342).

FDIC insurance does not protect against market losses due to selling CDs in the secondary market prior to maturity. The premium value of secondary buys is not insured. Insurance is only for par value plus accrued interest up to $250,000.

Need for specific return

There are several yield calculations to consider when evaluating a brokered CD. These yields are based on the coupon rate, the purchase price and the number of years until the CD's maturity or call date. Interest income from CDs is generally subject to income tax.

Yield to Maturity (YTM) represents the return an investor will receive if a CD is held to term. Annual Percentage Yield (APY) is also quoted and represents the return earned based on a simple interest calculation that includes the effect of compounding. Yield to Call (YTC) is the return earned if a CD is called prior to maturity. Current Yield (CY) measures the immediate return based on the CD's annual cash flow and its purchase price.

Since CDs may have multiple redemption scenarios (e.g., at maturity, by call or sale prior to maturity), the lowest of the YTM or YTC is quoted to the investor at the time of purchase.

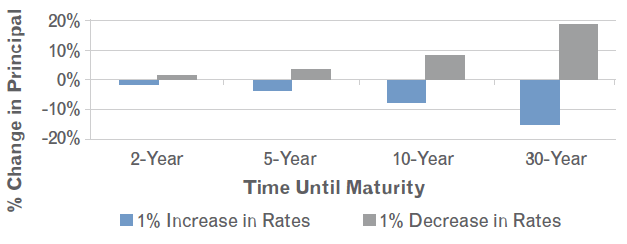

Interest rate effect on CD and bond valuesLiquidity and interest rate sensitivity

Raymond James and other broker/dealers, though not obligated to do so, may maintain a secondary market in brokered CDs. The secondary market may be limited and may be discontinued at any time without notice. CDs are intended to be held until maturity, as this assures redemption at par value. Investors may sell them before the stated maturity date, if needed, at prevailing market prices, and proceeds may be more or less than the original investment. Sales charges may apply.

However, there is no assurance that investors will be able to liquidate prior to maturity if a secondary market no longer exists. As with bonds, CD prices move opposite to interest rates, increasing when rates decline and falling when rates increase. Market values of longer-term CDs tend to be more sensitive to interest rate fluctuations. Thus, longer-term CDs are generally not suitable for investors with a short-term horizon. Other factors that may affect CD prices are order size, call features and investor demand.

Brokered CDs provide a reliable source of income and are protected by FDIC insurance.

How interest rates affect bond values

This chart is for illustrative purposes only and is not indicative of any actual investment.

In the event of bank failure

In the event that a financial institution becomes insolvent, one of three things may occur: Another institution may acquire the insolvent bank and keep the original CD terms, another institution may acquire the insolvent bank and set a new interest rate1, or the bank will be closed and FDIC will make payments on insured deposits. Investors’ access to funds will temporarily be limited and the investors will receive up to $250,000 for principal and interest accrued to the date the issuer is closed. Any unearned interest will not be paid. In these instances, Raymond James will submit the paperwork for you. Additionally, an investor may face reinvestment risk.

Banks additional prepayment option

In rare instances, an issuing bank may decide to prepay a CD's interest in full through the original maturity Banks Additional Prepayment Options date. In an instance where prepayment occurs, investors would receive all interest payments and principal balance prior to the stated maturity of the issue. Both non-callable and callable CDs can be prepaid. While prepayment occurs infrequently, it is a possibility. The primary risk involved with prepayment is that it may increase the investor's tax burden in the year the prepayment occurs.

1 If the institution changes the interest rate on a CD after acquisition, it must offer an optional redemption at par.

Managing interest rates

In most market conditions, long-term CDs offer higher yields than short-term CDs. By investing in short-term CDs, an investor has the ability to reinvest funds as rates go up, but will typically earn a lower rate of return associated with short maturities.

In contrast, generally long-term CDs offer higher rates, which, over their lifetimes, may or may not keep up with inflation or rising interest rates and, thus, may or may not provide the highest possible rate of return.

By “laddering maturities,”* investors can take advantage of reinvestment opportunities while potentially earning a higher overall return. A laddered CD portfolio is structured by purchasing several CDs with consecutive maturities. As each CD matures, the proceeds are reinvested in a new CD that has the next longest term on the ladder.

Although it is impossible to control or predict future interest rates, investors’ financial security may depend on the successful management of interest rates.

Advantages of buying brokered CDs through Raymond James

When investors purchase brokered CDs through Raymond James, they gain the convenience of recordkeeping. With consolidated recordkeeping, it’s easy to keep track of FDIC insurance limits. Combined statements mean less paperwork at tax time.

Brokered CDs are issued by banks via a “master CD” to deposit brokers who, in turn, offer interest in the master CD to individual investors. CDs are offered in electronic form without an actual certificate. All securities are held at the firm and are included on one monthly statement.

Before investing in a brokered CD

Investors should understand when the CD matures, how often it pays interest and how much interest it pays. Find out if the issuer has the right to call or redeem the CD prior to maturity. Compare the yields quoted versus those of non-callable alternatives. Understand secondary market liquidity in case it is necessary to cash out prior to maturity. Investors should check all their existing deposits at that bank prior to purchasing its CD so they won't exceed FDIC insurance limits. Finally, consider all risks and benefits and how this investment alternative may help meet investment objectives. Remember, brokered CDs may not be suitable for everyone.

Resources

- FDIC insurance information is available at fdic.gov.

- The U.S. Securities and Exchange Commission offers a guide, High-Yield CDs: Protect Your Money by Checking the Fine Print, at sec.gov/investor/pubs/certific.htm.

- A comprehensive overview of brokered CDs is also available at SIFMA’s investinginbonds.com.

* Should interest rates remain unchanged, increase, or even decline, a laddered approach may help reduce risk, improve yields, provide reinvestment flexibility, and provide shorter-term liquidity. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and durations.

The information contained herein has been prepared from sources believed reliable but is not guaranteed by Raymond James & Associates, Inc. and is not a complete summary or statement of all available data, nor is it to be construed as an offer to buy or sell any securities referred to herein. Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users or members.