Laddering Maturities

The investment strategy of laddering attempts to mitigate interest rate risk while blending short and long term bonds for an enhanced yield. The laddering or stepping of maturities can result in not only reduced risk and improved returns, but also permits reinvestment flexibility, a predictable cash flow and a desired level of liquidity. It is a strategy that takes the “guess” out of predicting future interest rates yet offers a partial hedge to future rising rates.

A laddered portfolio is structured by purchasing several bonds with differing maturities, for example: three, five, seven and ten years. As each bond matures, proceeds are reinvested in a new bond at the longer-term end of the ladder, which often is the highest yield within the desired maturity range. If interest rates are rising, the maturing principal can be invested at higher rates. If rates are falling, the reinvestment of proceeds will be at lower rates but the remaining ladder will still be locked-in and earning higher yields, helping to potentially smooth out the income generated by the portfolio. Bond ladders containing non-callable bonds may be more predictable as the term of investment is fixed and will not change. Some examples of various ladder structures are listed below.

- Check-a-Month

Since most bonds pay income on a semi-annual basis, selecting six specific bonds that pay interest in different months will create a monthly stream of income to supplement other income or provide an opportunity for reinvestment. Portfolios of individual bonds can be customized to meet individual income requirements. - Systematic Investing

Investors who do not have sufficient funds to build a complete ladder, but can save enough for a rung each year, should begin in the middle and add positions on either side in subsequent years. For long-term investors, systematic investing also provides the ability to take advantage of swings in interest rates. - Barbells

Barbells are a bond investment strategy similar to laddering, except that purchases are concentrated in the short-term and long-term maturities. This allows the investor to potentially capture high yields from longer maturities in one portion of their portfolio, while using the shorter maturities to minimize risk. Barbells can provide opportunity in both rising and declining interest rate environments: If interest rates decrease, the long end of the barbell provides potential for capital gain, however, you would be reinvesting the proceeds into potentially lower yielding bonds. If interest rates increase, the shorter end of the barbell can be reinvested at the new higher rates, however, the current market value of existing long term bonds could decline.

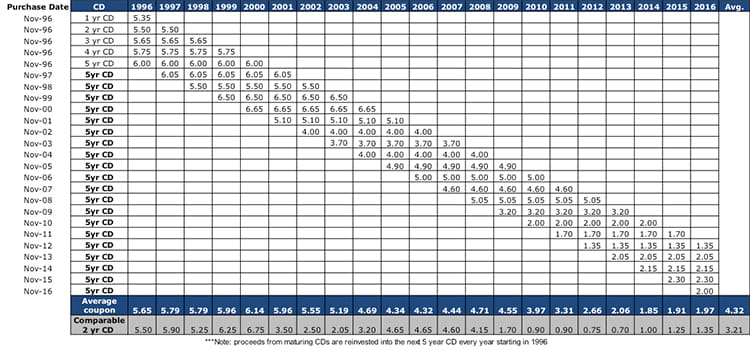

A Historical Example: Laddering Certificates of Deposit

The following example demonstrates that laddering maturities is a time-honored strategy that can both lessen interest rate risks and potentially optimize the performance of the overall bond portfolio. The table below compares the historical 2-year CD versus a ladder of CDs that is rolled periodically. This hypothetical portfolio had an approximate duration of 2.5, meaning that it would decline (appreciate) by 2.5% for every 1% move up (down) in interest rates. Please note that FDIC insured brokered certificates of deposit differ from bank CDs. If an investor chooses to redeem a bank CD prior to the stated maturity, they will pay an interest penalty. With a brokered CD, if the funds are needed prior to maturity, the CD is sold on the secondary market. Proceeds may be more or less than the original investment.

Historical Bond Ladder – Brokered Certificates of Deposit (CDs)

(Source: Raymond James) This example is for illustrative purposes only. The analysis would be different if compared to CDs of other maturities. Past performance is not indicative of future results. Investing always involves risk and you may incur a profit or loss. No investment strategy can guarantee success.

Interest Rate Considerations

Interest rates should play a key role in the investment decision-making process. For example, if interest rates are higher than in recent years, investors may decide to invest all of their assets at one time. On the other hand, if interest rates are lower, investors may decide not to invest, anticipating missed opportunities for a greater return should interest rates increase in the future. Although investors cannot control, or even predict interest rates, their financial security may depend on the successful management of them.

Laddering maturities can provide results in any one of three ways:

- If interest rates stay the same, yields will be higher as, during reinvestment, money is shifted into longer-term investments. Historically, long-term bonds possess a higher yield than shorter-term bonds.

- If interest rates rise, the investor will participate in higher yields, as bonds in their portfolio mature and principal is returned investors can reinvest at the higher yields.

- If interest rates fall, investors’ portfolios may benefit from a stable overall return due to higher rates locked in with earlier investments.

Conclusion

This time-honored investment technique, in which an investor blends several bonds with differing maturities, provides the benefit of blending higher long-term rates with short-term liquidity. Should interest rates remain unchanged, increase, or even decline, a laddered approach to fixed income investing may help reduce risk, improve yields, provide reinvestment flexibility, and provide shorter-term liquidity.

Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration.

There is an inverse relationship between interest rate movements and bond prices. Generally, when interest rates rise, bond prices fall and when interest rates fall, bond prices rise.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Past performance is no assurance of future results.

Diversification does not ensure a profit or protect against a loss. Investments are subject to market risk, including possible loss of principal. This communication is intended to improve the efficiency with which Financial Advisors obtain information relevant to their client's taxable fixed income holdings. This information should not be construed as a directive from the RJ&A Taxable Fixed Income Department to buy or sell the securities noted above. Prior to transacting in any security, please discuss the suitability, potential returns, and associated risks of the transactions(s) with your Raymond James Financial Advisor.

The information contained herein has been prepared from sources believed reliable but is not guaranteed by Raymond James & Associates, Inc. (RJA) and is not a complete summary or statement of all available data, nor is it to be construed as an offer to buy or sell any securities referred to herein. Trading ideas expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation or needs of individual investors. Investors are urged to obtain and review the relevant documents in their entirety. RJA is providing this communication on the condition that it will not form the primary basis for any investment decision you may make. Furthermore, because these are only trade ideas, investors should assume that RJA will not produce any follow-up. Employees of RJA or its affiliates may, at times, release written or oral commentary, technical analysis or trading strategies that differ from the opinions expressed within. RJA and/or its employees involved in the preparation or the issuance of this communication may have positions in the securities discussed herein. Securities identified herein are subject to availability and changes in price. All prices and/or yields are indications for informational purposes only. Additional information is available upon request.